Key Takeaways

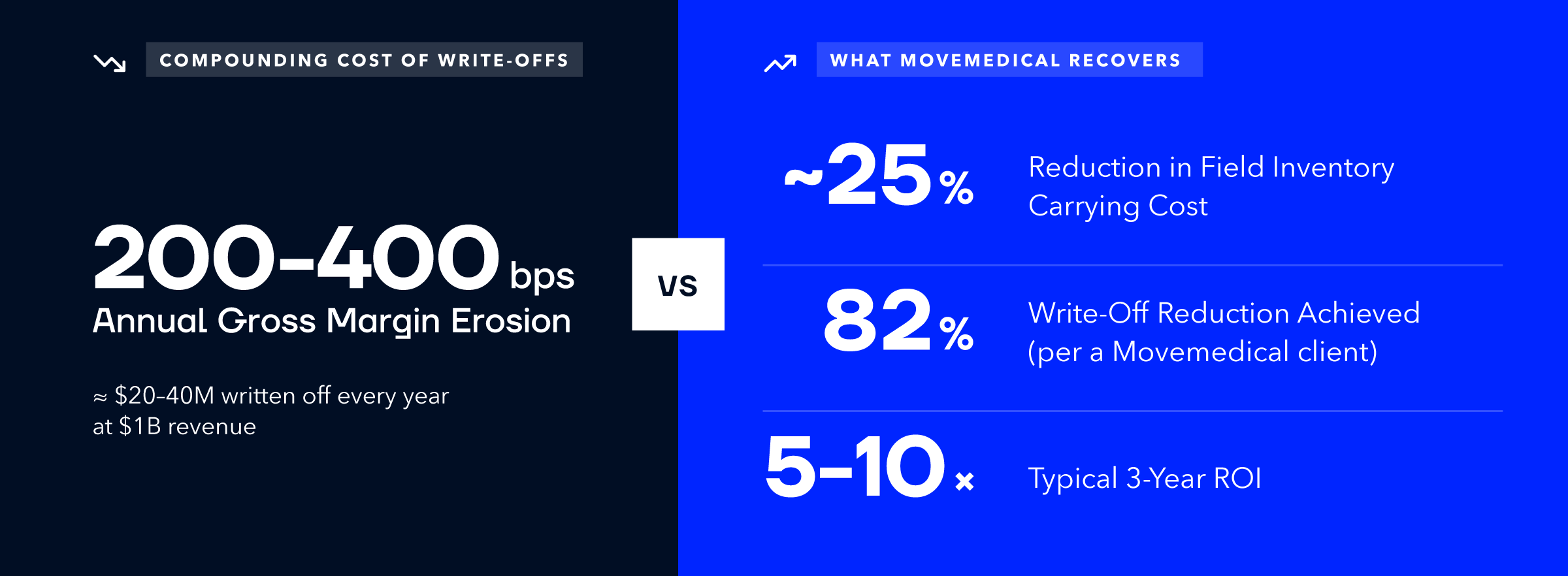

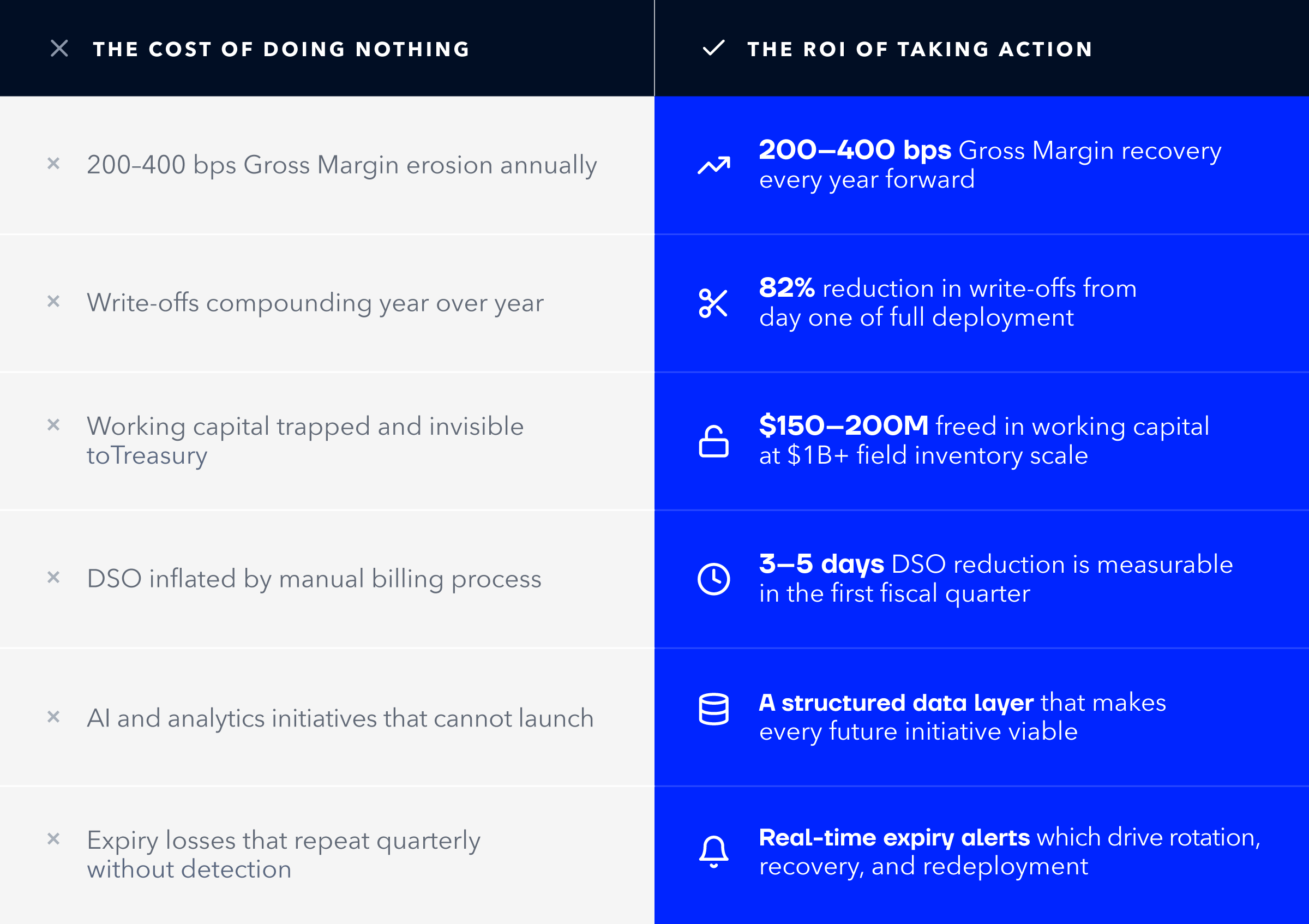

- MedTech manufacturers without field inventory intelligence absorb 200–400 basis points of preventable gross-margin erosion every year — showing up as write-offs, expired product, and unbilled cases, not as a line item.

- The three costliest, least-tracked field liabilities are inventory shrinkage, avoidable expiry losses, and uncaptured bill-only revenue — each measurable, recurring, and preventable.

- "Doing nothing" is not a neutral financial position. Every quarter on the status quo compounds working-capital, DSO, and carrying-cost losses.

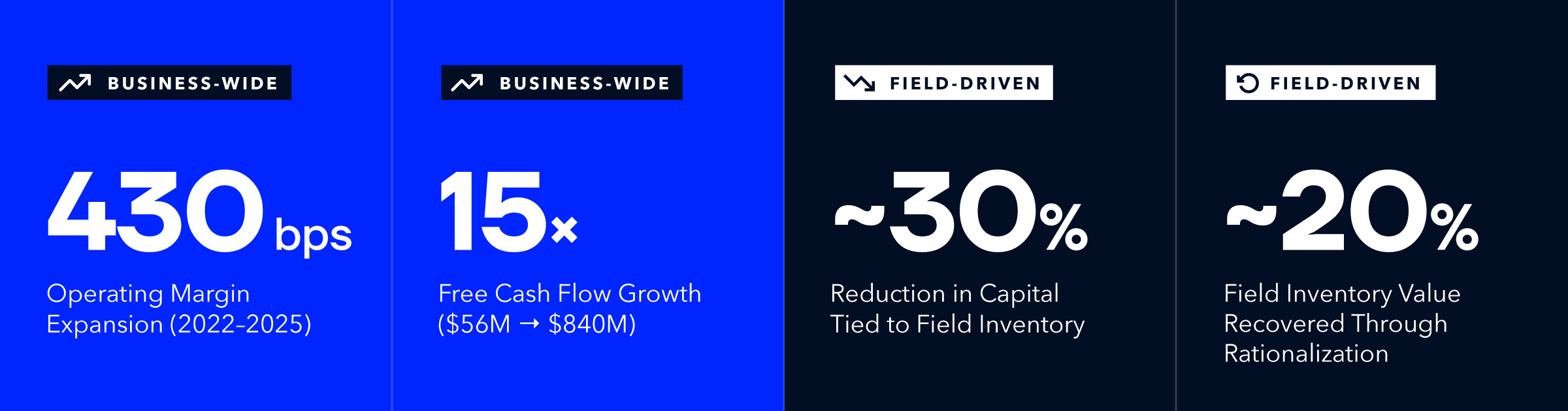

- Smith+Nephew's public turnaround — anchored on inventory and working-capital discipline — delivered a 430 bps operating-margin expansion and a 15× free-cash-flow increase, proving this is a board-level financial event.

- Movemedical is the field inventory management platform built for this problem. Its complimentary EBITDA Audit quantifies your specific field-supply-chain friction and delivers a board-ready 3-year NPV model built on your data.

Every quarter that a medical device company operates without field inventory intelligence, it absorbs preventable losses. Write-offs, expired product, untracked consignments currently compound silently on the P&L. This is not a technology problem. It is a financial problem. And the cost of doing nothing is far larger than most CFOs have ever quantified.

The Conversation Finance Is Not Having

Ask most CFOs at a medical device manufacturer how much inventory they have in the field right now, and they will give you a number from their ERP. That number is wrong.

The ERP knows what products left the warehouse. It does not know what is sitting in each sales rep’s trunk, what expired on a hospital consignment shelf last month, or what product was used in an OR three weeks ago and never reconciled into a bill-only event. That gap is not a data anomaly. It is a recurring financial liability.

For enterprise-scale MedTech operations, the cumulative impact of unmanaged field inventory is a 200–400 basis point drag on Gross Margin annually. At a $1 billion revenue company, that is $20–40 million per year in preventable loss. Not from market headwinds. Not from competitive pricing pressure. This is strictly from operational friction that has simply never been measured.

Three Places Your P&L Is Bleeding Right Now

Field inventory losses in medical device are not random. They concentrate in three predictable categories, each of which is measurable, recurring, and preventable.

1) Inventory Write-Offs and Shrinkage

Field inventory that can’t be located is eventually written off. In a manual environment, this happens through unreconciled rep-to-rep transfers, consignment adjustments that never get documented, and product that disappears from hospital storage without a usage record. None of these events are intentional. They are the natural output of a system that has no real-time chain of custody.

Organizations that have implemented field inventory intelligence have reduced write-offs by as much as 82%. At enterprise scale, the financial impact of that single improvement can fund years of platform investment.

2) Expiry Losses That Were Entirely Avoidable

Product expires in the field because no one knows it is there. Implants sit on hospital consignment shelves past their expiry dates. Loaner kits cycle through rotations without anyone tracking the age of the components. By the time the expiry is discovered, the product is unrecoverable, unrecyclable, and uncompensable.

With real-time field visibility, expiring product can be identified well in advance, rotated to higher-velocity accounts, or recalled to the warehouse for use elsewhere. The write-off becomes a recovery. The loss becomes a redeployment. The difference is visibility.

3) Revenue That Never Gets Captured

The gap between surgical case and invoice is one of the most significant and least-examined friction points in the MedTech revenue cycle. When bill-only capture relies on manual documentation, product usage records are incomplete, paperwork is delayed, and weeks pass before finance can generate an accurate invoice. Every day of that delay inflates your Days Sales Outstanding. Every disputed invoice is revenue at risk.

Automated bill-only capture reduces DSO by 3–5 days across a $1 billion revenue business. That is a measurable improvement in cash conversion that analysts and board members notice.

What “Doing Nothing” Actually Costs

The status quo is not free. It carries a recurring cost that simply does not appear as a line item. It appears as write-offs in the annual audit. It appears as inventory carrying costs inflated by safety stock that would not be necessary if the field were visible. It appears as working capital trapped in field assets that Treasury cannot see, cannot optimize, and cannot deploy.

Why the ERP Is Not Enough

A question that frequently arises: “Why can’t the ERP just handle this?”

ERPs are designed to manage enterprise transactions. They track purchase orders, general ledger entries, and warehouse movements with precision. What they are not designed to do is follow an implant from a distribution center to a sales rep’s trunk to a hospital consignment shelf to an OR table — in real time, with a clear chain-of-custody accountability at every step.

The medical device supply chain is not a warehouse problem. It’s a last-mile problem. It operates through distributed networks of agents, distributors, and independent reps, each with their own workflows, stocking models, and hospital relationships. The ERP records what the system is told. Field inventory management records what actually happened. Those are not the same thing.

Movemedical does not compete with your ERP. It completes it. The structured, standardized operational data that Movemedical generates is what makes ERP data trustworthy at the field level, and makes future investments in AI, predictive analytics, and demand planning viable.

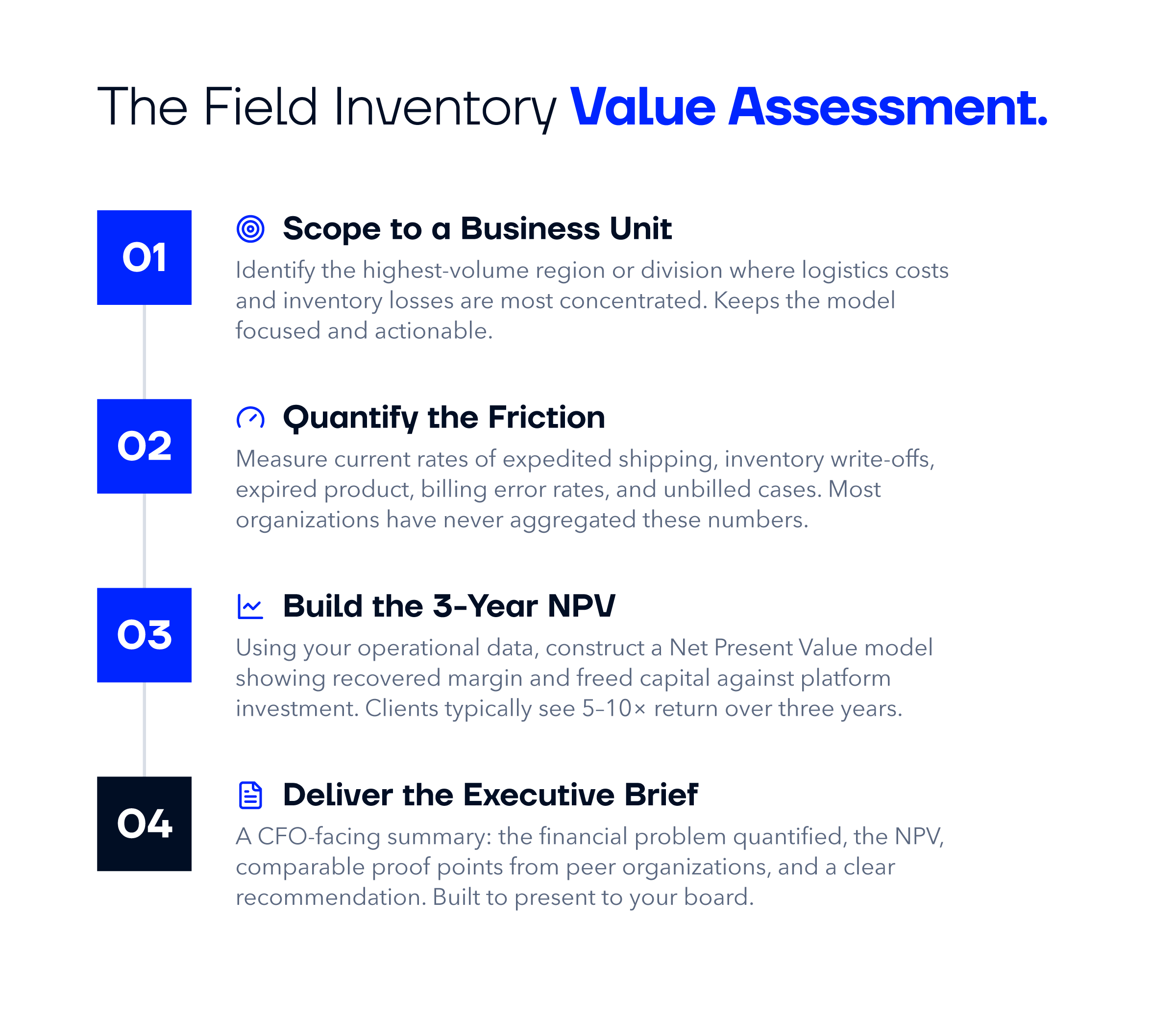

What a 3-Year NPV Model Actually Shows

Abstract claims about ROI are not useful to CFOs. Specific financial models built on actual operational data are.

Movemedical’s Field Inventory Management Value Assessment is a scoped financial diagnostic that quantifies the specific friction in your field supply chain and translates it into the metrics your board already tracks. It’s not a product demo. It’s not an industry-average benchmark exercise. It’s a model built from your data, scoped to a high-volume business unit or region where the opportunity is largest.

What the Market Is Already Telling You

If there is any remaining doubt that field inventory discipline belongs on a CFO’s agenda, consider what one of the world’s largest medical device companies has been telling its board, its analysts, and its shareholders for the past three years.

Smith+Nephew, a $6 billion global MedTech manufacturer operating across Orthopedics, Sports Medicine, and Advanced Wound Management, launched a multi-year operational transformation in 2022. The centerpiece of that transformation was a disciplined focus on exactly the levers this article has described: inventory management, working capital discipline, and asset utilization.

The results are now public record.

Smith+Nephew’s leadership told investors in their most recent annual report that this transformation was built on “working capital discipline and asset utilization,” “improving inventory management,” and “increased rigor and discipline in capital allocation,” including explicitly improving inventory set turn by deploying sets more deliberately across the field.

Their RISE strategy, announced for 2028, targets an adjusted Return on Invested Capital of 12–13% — a number their leadership has directly linked to releasing the capital trapped in field inventory. The $500 million in working capital they expect to freethrough inventory rationalization is not incidental to their growth strategy. It is a funding mechanism for it.

Smith+Nephew is a peer organization. Their board faces the same pressures, the same analytical scrutiny, and the same capital allocation decisions that yours does. When a company of this scale makes inventory management a board-level priority — and delivers a 15× increase in free cash flow as a result — the question for every other CFO in MedTech is not “is this relevant to us?”

The question is: how long can we afford to wait? Schedule your Field Inventory Management Value Assessment and find out exactly what your field operations are costing you — and what they could be returning.

About the Author